When it comes to finding the best mortgage rate, many are left confused. This is especially true with first-time buyers who may not know how to go about qualifying for a mortgage. That’s why, we’ve outlined the steps you should take below to find the best mortgage rates. That way, you can ensure a smooth home buying process.

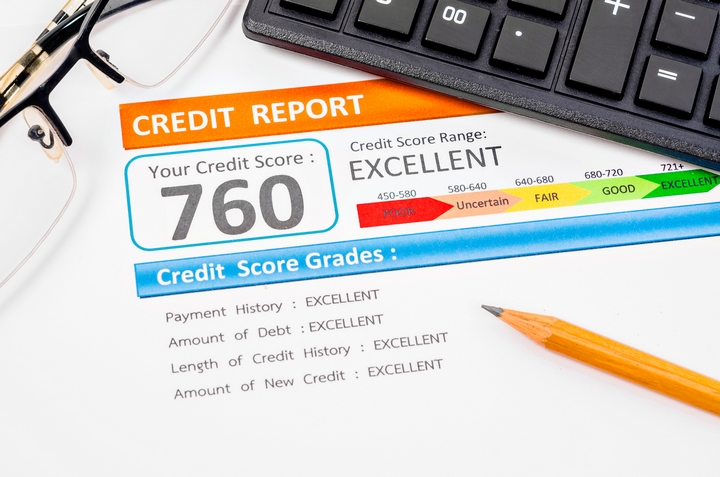

1. Know Your Credit Score

Prior to approaching a lender for advice, you should know what your credit score is. If your credit score is low, chances are you will not be approved for a large amount. You should ensure that you’re credit score is in the range of ‘good’ to ‘excellent’ to make sure you are being approved for the highest amount possible. Knowing your score prior to speaking to lenders can also help to prepare you for any disappointment. First-time buyers often overlook this important factor and are left dealing with the consequences.

2. Educate Yourself

Prior to getting a mortgage, you should be prepared to educate yourself on the process and different types available. If you do not understand the process, you may be left confused or frustrated in the future. The two different types of loans available are often grouped into two separate categories conventional loans, and government-backed loans. Conventional loans are provided by private lenders (banking institutions, thrift institutions or others) while a government backed loan is insured by the government. Knowing which type you prefer, and which you are likely to get more money from, can help you make the decision when shopping for a loan.

3. Contact Multiple Lenders

When shopping for a loan, it is vital to contact multiple lenders. Depending on which institution you go to, you may be approved for different amounts. Rather than sticking to the first lender or amount you get approved for, you should apply to multiples to ensure you are getting the highest amount.

4. Consider Additional Costs

If you decide to work with a mortgage broker, you may have to pay an additional fee for them to work with you. As well, there may also be underwriting fees, settlement fee’s and closing costs that you need to consider before getting a mortgage. Before you decide on the mortgage rate to go with, you should also take into consideration any additional costs.

5. Research the Lenders

Before you decide to work with a lender, you should research the company. If the company does not have favorable reviews, or are not highly regarded then you should consider looking else ware. Also take into consideration the lenders cost and customer service as it can drastically impact your borrowing experience.

6. Read the Contact

Before you agree to signing on with a lender, you should read the contract and understand exactly what is expected from you. If you do not understand the contact you are signing you should speak to your lender for them to clarify. Knowing exactly what you are signing up for prior to purchasing can save you time, costs and frustration later on.

7. Understand Your Financing Options

Be sure that you understand the type of financing you are getting, prior to signing an agreement with a lender. Financing can be categorized into two categories as either fixed rate mortgages or adjustable- rate mortgages. A fixed rate is typically viewed as a less volatile situation as you will know the rate you will be paying throughout the term. But, with an adjustable rate-mortgage your payments may fluctuate which can result in either higher payments or lower payment.